Actively Managed Funds: Are Any of Them Worth It?

Is it possible to find and invest in actively managed funds that consistently beat the market?

Happy Friday morning everyone! I hope everyone has had a wonderful week. If you’ve been enjoying my newsletter, another newsletter you might like is Walt Hickey’s Numlock News. Before subscribing to Walt’s newsletter, I was under the impression that I knew everything; his newsletter proves me wrong every morning. Did you know that 33% of Americans who trade in their car for a new one are underwater on their loan, and end up taking out a loan for more than their new car is worth? Learn a bunch of interesting facts like these every morning by subscribing to Walt’s newsletter.

Today’s topic was recommended to me by one of the faithful readers of Time & Money. He wanted to know if there are any actively managed funds that are worth investing in. It’s common knowledge that index funds outperform active funds most of the time, but are there any actively managed funds that consistently beat the market? Read on to find out.

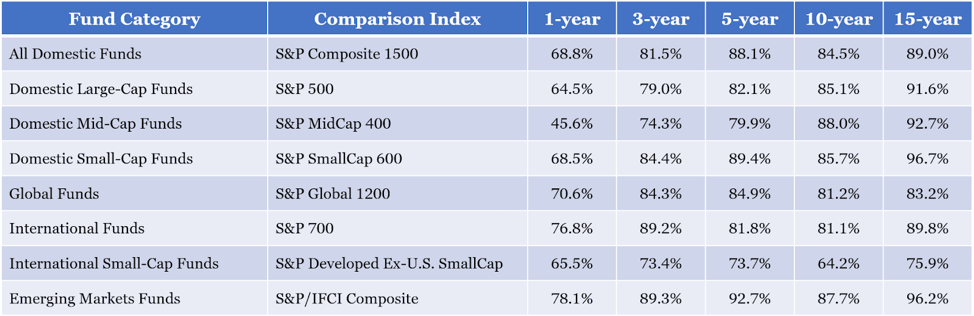

Amongst savvy investors, it’s now common knowledge that index funds generally outperform actively managed funds. For the first time, investors now have as much money in index funds as they do in actively managed funds. Passive investing is now seen as the best way to build wealth long-term, and performance of index funds prove that. The table below shows the percentage of actively managed funds that underperformed their respective indexes.

Percentage of Equity Funds Outperformed by Benchmarks

Are there any good actively managed funds?

When only looking at periods of time greater than one year, index funds outperform actively managed funds in every category. We know that the odds are slim when it comes to picking an actively managed fund that beats the market, but can it be done? Are there actively managed funds that consistently beat the market?

Look for low expenses

Actively managed funds with lower expenses perform better than those with higher expenses. Research by Moneyshows that active funds with expenses in the lowest quartile (bottom 25%) returned 9.4% per year over the last 5 years. Active funds with expenses in the highest quartile returned only 4.4%. There appears to be a direct correlation between how much funds are charging and how much they are returning. Funds that charge the most have the poorest returns.

Can brilliant investors beat the market?

Jeffrey Gundlach is, by many accounts, a fantastic bond investor. He foresaw the subprime mortgage collapse, calling it an “unmitigated disaster” in June 2007. His biggest fund has consistently outperformed the index benchmark since its inception. The fund he managed before starting his own company consistently outperformed its peers, too.

However he has also been very wrong in the past. Gundlach said that “munis [municipal bonds] are the new subprime” in 2011, and reportedly liquidated most of his holdings in municipal bonds. The decline he predicted didn’t occur, and prices instead kept going up. Earlier this year, he predicted the 10-year Treasury yield would be 6% by 2021. That’s still possible, but the yield is now much lower than it was at the beginning of the year, and 6% by 2021 is pretty ambitious.

Gundlach’s funds have performed well for the most part, but he clearly can’t predict the future. Beating the market consistently almost requires you to be able to see into the future, or at the very least have very good luck. I’m not sure what percentage of Gundlach’s success has been clairvoyance and how much has been luck, but I don’t think we can say with any degree of certainty that he will continue outperforming the market in the future.

The holding company run by Warren Buffett, Berkshire Hathaway, has returned 20.8% per year since 1965. Over the last 15 years, though, Berkshire returns have slightly lagged the S&P 500. Some speculate that Warren Buffett has lost his touch, but I think something else is going on: it’s harder than ever to beat the market.

Buffett made a bet in 2007 with a hedge fund firm that an S&P 500 index fund would outperform the basket of hedge funds his competitor chose. The bet was a decade long, and it wasn’t even close: Buffett’s index fund returned 7.1% annually and the hedge funds returned 2.2%. On investing in index funds, Buffett says “I think it’s the thing that makes the most sense practically all of the time.” Though he has outperformed indexes in the past, it’s clear that Warren Buffett is now a huge fan of passive investing.

Are investors getting smarter or are actively managed funds getting worse?

The amount of money flowing into index funds either means that investors are finally waking up and getting smarter or index funds have only recently started outperforming actively managed funds. It appears to be the former. Studies published as far back as 1968 have claimed that actively managed funds are inferior to their respective benchmarks.

A study published in 1999, looking at mutual fund performance from 1975-1995, actually found some evidence of stock-selection skills. The study found that stocks mutual funds actively bought significantly outperformed stocks they sold by about 2% in the year following the trades. They did not, however, find that stocks widely held by funds outperformed other stocks.

I think it’s important to highlight what that 1999 study found. They found evidence of stock-picking ability, but the overall returns of actively managed funds weren’t better than returns of index funds. Why is that?

It’s about the taxes

Picking stocks that can outperform stocks you already have over the short-term (the study only looked at the year after stocks were bought or sold) is only half the battle. When a stock is sold, you have to pay taxes on the gains. If you’re constantly buying and selling stocks, you can rack up a significant tax bill (assuming the stocks went up in price). Short-term capital gains (on assets held less than one year) are taxed at regular income tax rates, which can be significantly higher than long-term capital gains tax rates.

The evidence in the 1999 study and the data from SPIVA show that active fund managers have a better chance at outperforming benchmarks over a short period of time (although their “ability” is still very questionable). Even if active funds can “beat the market” in the short-term, the taxes they generate in the process likely make those returns not worth it. If short-term capital gains were taxed at the same rate as long-term capital gains, it might be a different story.

Survivorship bias

Actively managed funds that perform poorly don’t survive and are usually quickly forgotten. The funds that survive are the ones that perform the best, and the ones we remember. The SPIVA data, in the table at the beginning of the article, eliminates survivorship bias and includes all funds. When choosing an investment strategy, it’s important to look at the performance of all funds, not just one or two outliers that may have outperformed benchmarks.

The 1999 study (I promise this will be the last time I reference it) also found that past performance was only weakly correlated with future success. This means that the performance of all active managers is a better barometer of future success than only looking at the ones that have been successful in the past, like Jeffrey Gundlach.

The bottom line

If you look hard enough, you can find a handful of funds that have beaten the market over longer time periods, like 10 or 15 years. Beyond that, it becomes nearly impossible to find an actively managed fund that has consistently outperformed index funds.

Even investors like Warren Buffett have struggled to outperform index funds recently (as I mentioned earlier, the 15-year performance of Berkshire Hathaway slightly lags the S&P 500). There’s no doubt there will be some fund managers who outperform the market over the next 10 or 15 years, but who are they? I don’t think anyone knows the answer to that question. Our civilization is pretty advanced, but we haven’t yet figured out time travel.

The numbers show that active investing is, more often than not, a losing strategy. Picking active funds with low expenses or historically successful managers may improve your odds, but your chances are probably better with index funds. When it comes to choosing where to invest a lifetime’s worth of savings, it’s probably smarter not to play the odds.

Disclosure: I do not own shares in any of the funds/companies mentioned in this article.

Thanks so much for subscribing to my newsletter! If you’re new, take a minute to dig through the archives for posts like How Do I Start Investing? or How to Pay Off Debt.

If you’re enjoying the newsletter, forward it to someone you think may enjoy it too! They can subscribe by clicking the handy button below.